In time series forecasting, two Triple Exponential Smoothing methods are used widely Triple Exponential Smoothing Average (TEMA) and Holt-Winter’s utilize different methods to smooth out the values and enable accurate forecasting. However, these key differences between the two methods have an impact in the final forecast. TEMA is a simpler method that uses three weighted averages to smooth the data, whereas Holt-Winters is a more complex method that takes into account both trend and seasonality.

Holt-winters Triple Exponential Smoothing

Holt-Winters method extends the concept in double exponential smoothing to account for three attributes Trend, Level and Seasonality of the data. It employs three smoothing factors, one for the level (α – alpha) , one for the trend (β – beta) and one for seasonality (Ɣ -gamma). All three are

Formulae :

Level (Lt)

Lt = α * (Yt – St-m) + (1 – α) * (Lt-1 + Tt-1)

Trend (Tt):

Tt = β * (Lt – Lt-1) + (1 – β) * Tt-1

Seasonality (St):

St = Ɣ * (Yt – Lt) + (1 – Ɣ) * St-m

Forecasting:

Forecast for time t + h (Ft+h) = (Lt + Tt )* St-m

For detailed explanation refer “https://wisdomschema.com/blog/comparison-of-dema-holt-winter-double-exponential-smoothing/”

Triple Exponential Moving Average

Triple Exponential Moving Average (TEMA) extends the standard Single Exponential Smoothing by applying the Exponential Moving Average (EMA) values thrice. Three levels of EMA applied on the data set provides better smoothened and accurate forecasts.

Refer detailed Double Exponential Smoothing Average blog “https://wisdomschema.com/blog/comparison-of-dema-holt-winter-double-exponential-smoothing/”

Dataset Information

Two different datasets were used to illustrate the differences between two methods

Industry dataset : Erratic Trend

The sample dataset from the Industry schema is as follows, with a focus on the “salesorderheader” relation.

Field

Type

Candidate Variable

OrderID

Character

CustomerID

Integer

ShipDate

Timestamp

✔

SalespersonemployeeID

Integer

ShipMethodID

Integer

TerritoryID

Integer

SubTotal

Numeric

✔

Number of records : 1561

Candidate keys

Number of unique values

Max Value

Min Value

Subtotal

623

129,261.254

2.29

ShipDate

675

2014-05-01

2011-06-01

2.Weather dataset : Visible Trend

Field

Type

Candidate Variable

Date

Timestamp

✔

temperature

numeric

✔

idx

Integer

✔

Number of records : 216

Candidate keys

Number of unique values

Min Value

Max Value

temperature

195

18.25

32.19

ShipDate

216

2000-01-01

2017-12-01

Workflow

Industry dataset

Weather dataset

Reading & Manipulating Data

Industry

The data is read via DB connector node and fed into KNIME via DB reader after choosing appropriate relation and extracting the necessary primary candidate key.

SubTotal (i.e. measure) values are grouped by applying an aggregate function (SUM), and this grouping is based on month and year.

Weather

The data is stored in an excel and the data is read via the Excel reader node and fed into the KNIME

Forecasting

Industry

Execute the Triple exponential smoothing methodology on the data present in the “SubTotal” column using a standard node called “moving average”.

Entire calculation for Holt-Winter method is performed using SQL delegated to backed in database by executing a database procedure using “DB Query Executer”

Weather

TEMA is calculated with the help of “moving average” node and the window size is chosen accordingly

The Holt-Winters method was implemented in Excel, and the results were imported into KNIME for further processing.

Visualization

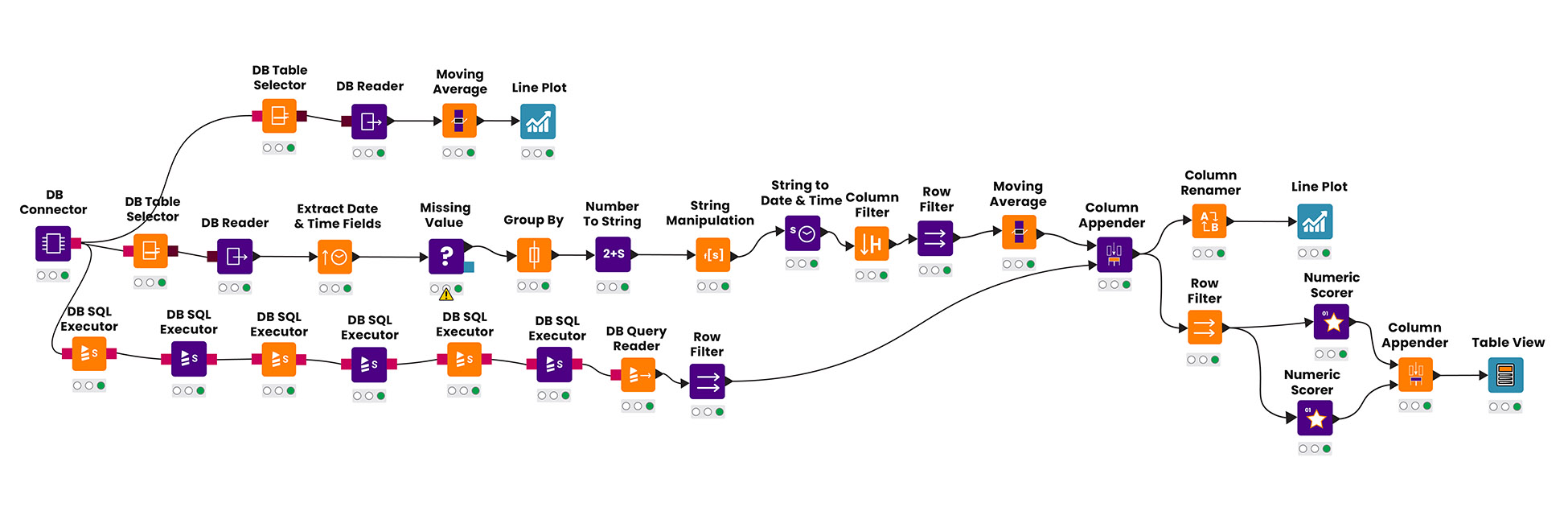

1. Industry dataset

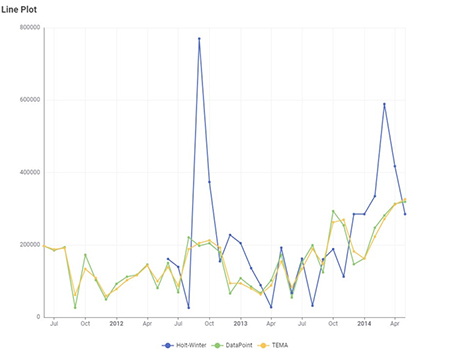

2. Weather dataset

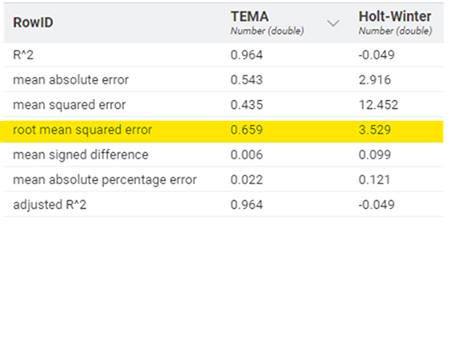

Forecast Accuracy

1. Industry dataset

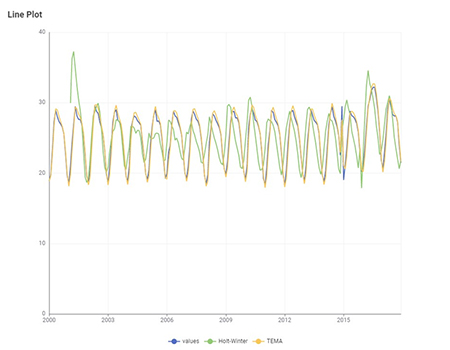

The Root Mean Square Error value of Holt-Winter is very high, which in turn means the accuracy is very low

This because there is no plausible trend and seasonality in the dataset

Holt-winter method is not effective when trends or seasonality is erratic in nature

2. Weather dataset

The Root Mean Square Error value for Holt-Winter is very low compared to the RMSE value of the industry dataset

RMSE value is low, which means the accuracy level is high

This is due to the presence of trend and seasonality

Summary

TEMA is ideal for datasets where patterns are driven mainly by the trend, and there are no significant seasonal variations.

It is efficient when dealing with data without repeating cycles or where seasonal effects

Holt-Winters tends to provide more accurate forecasts when the historical data shows consistent seasonal patterns.

By considering both trend and seasonality, it can model and predict future values in a way that reflects the underlying patterns in the data.

If the data lacks seasonal patterns, TEMA might yield simpler and accurate results. On the other hand, if seasonality is evident, Holt-Winters is the preferred choice for reliable forecasts.